Health & Fitness

Deficit Reduction - Time to Drop the Analogies, Stupid

America's foreign investment in nearly as large as the debt and is is growing faster than the cost of maintain the debt. So enough already with lame analogies about balancing the family budget.

In terms of policy battles, almost none have been as rancorous and heated as the 2011 debate to raise the federal debt ceiling that nearly shut down the federal government.

And while most politicians agree with balanced budgets in principle, the approach taken on each side of the aisle is very different.

Progressives argue for increases in personal tax rates while conservatives demand cuts to services.

Find out what's happening in Sussexwith free, real-time updates from Patch.

To support the latter, GOP representatives often spin the simple tale of a family on a tight budget. If expenses are too high or someone loses a job then of course spending cuts are required.

The art of persuasion

This down-on-your-luck family analogy has played well with voters. It’s concise. It’s easy to understand. And everyone — with the possible exception of the ever-more wealthy members of congress — can quickly relate to the central cost-saving message.

Find out what's happening in Sussexwith free, real-time updates from Patch.

This last point should be obvious to most of you since median wages for the middle class have been dropping for nearly two decades while executive compensation has been sky-rocketing.

A cynic might conclude that the analogy was chosen specifically by political/electoral operatives to reach the ever-expanding working-poor demographic — but I digress.

It’s an insulting comparison

There’s another feature about this analogy that makes it perfect for political persuasion: it assumes that the electorate is either too stupid or too emotionally invested in the political dichotomy that is modern American politics to process even the most basic financial analysis.

Perhaps that sounds harsh, but put yourself in the situation of having, for example, a mortgage you can no longer afford, medical expenses to pay or kids to put through college.

Only a damn fool would conclude that life must dramatically and immediately change to meet these unexpected financial challenges.

I prefer to give the public more credit than these politicians who — by the very nature of American politics — are beholden primarily to the special interest groups that fund the modern electoral process.

One size does NOT fit all

What about relying on savings while looking for new work? Seems like a sensible thing to do.

How about negotiating with your mortgage lender for a better rate? When faced with default, banks can be surprisingly flexible.

Maybe you need to swallow your pride and borrow some money from family and friends, or take a loan against some of your existing assets or go back to school for additional training or retraining.

I hear you can sometimes get paid to be retrained!

The point I am illustrating is that every family in a financial crisis has options. Some families will have more or better options than others, but every family will need a solution that is tailored to their specific situation.

Surely some families will need to cut expenses, file for bankruptcy and/or lose their homes. But proposing immediate and severe spending cuts as a one-size-fits-all solution should come as an insult to any self-respecting taxpayer.

Government is complicated ... by design!

In addition to the idiotic simplicity of the analogy, let’s also remember that the federal government is A LOT MORE F#@?ING COMPLICATED than a personal family budget.

That’s right, I said it!

The whole purpose of creating government is to have a large enough system to do big things like putting a man on the moon, creating integrated networks for moving cars, trains and electricity or building a hydroelectric dam.

And by creating a super-sized ‘family’ of over 300 million people, the US government can respond to a financial crisis with a wide variety of tools of which spending reduction is just one.

A history of debt

And better yet, America has a great history of managing debt. As Nobel Prize winner and Professor of Economics, Paul Krugman, wrote on Sunday about World War II:

“Taxpayers were on the hook for a debt that was significantly bigger, as a percentage of G.D.P., than debt today...”

“[Yet] ... the debt didn’t prevent the postwar generation from experiencing the biggest rise in incomes and living standards in our nation’s history.”

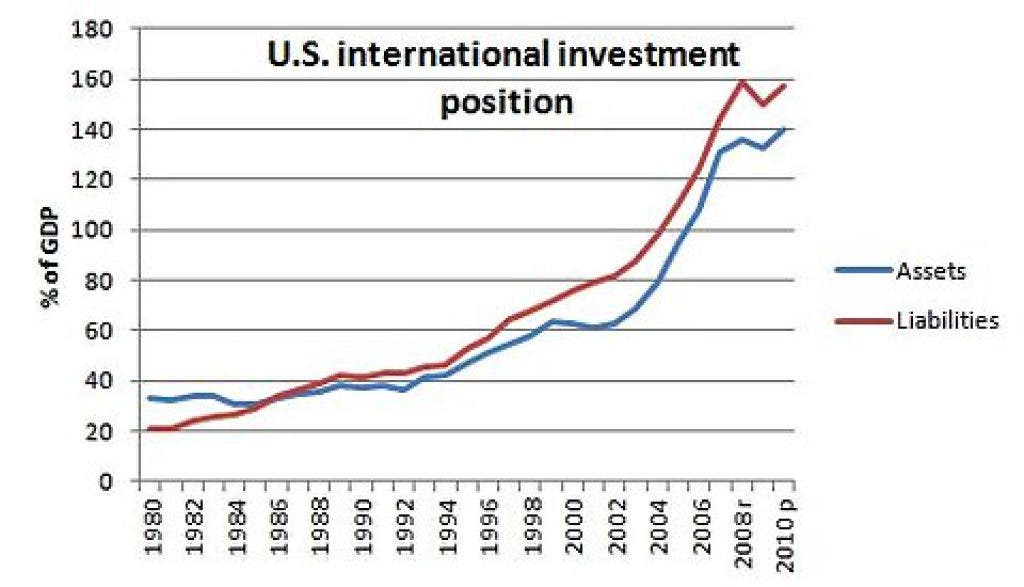

Unlike that time, American debt is now mostly foreign-owned. However, our overseas investments nearly match our liabilities.

That’s right, our investments nearly match our debts!

What’s more, yields on these assets consistently out-perform the costs we pay to borrow from foreign lenders.

Sounds complicated? Let me make my own family budget analogy to help you understand.

If you own a home or car, you might have a loan with a 6% interest rate. You might also have a mutual fund that pays, on average, 9% annually.

Should you be worried about your 30-year mortgage debt or 5-year car payment and pay off your loan as quickly as possible?

While paying down debt may feel better, investing the same amount of money in your mutual fund will cover the interest on your loan and your savings will still increase by 3%.

In this most simple of comparisons, America is in debt, but it’s on track to have more foreign investment than foreign liabilities.

Thus, only a damn fool would be hysterical about deficit reduction right now, especially when unemployment is so high.

Don’t insult my intelligence

As we all look forward to 2012 and beyond, what does this mean for the simpleton politicians — on the left and the right — who use quaint analogies to pull the wool over the eyes of the electorate?

How about an adult conversation and less rhetoric?

How about real solutions to our pressing problems of low employment and a failing education system.

How about compromise instead of political grid lock. Wouldn’t tax reform be an excellent compromise between spending cuts and increased taxation?

How about NOT spending 30% of your time raising money for the next election cycle!?!

Give us something — anything — but please, Members of Congress, no more analogies that insult our intelligence and expose your own ignorance of global economics.